If you’re anything like me, you’ve probably heard the terms “blockchain” and “cryptocurrency” buzzing around like busy bees in the tech world.

Stick with me, and we’ll embark on a journey to unravel this enigma together.

Imagine a world where transactions are transparent yet secure, where trust is not a luxury but a given.

Sounds too good to be true?

Well, that’s the magic of blockchain technology for you.

It’s like the secret sauce that makes the complex world of digital currencies not just a fantasy but a tangible reality.

And here’s where it gets interesting.

Cryptocurrencies, with Bitcoin leading the charge, are not just digital assets floating in cyberspace.

They are meticulously crafted, thanks to the robust architecture of a blockchain network.

We’re about to dive deep, exploring the intricate dance between blockchain technology and cryptocurrency, demystifying the complexities, and unveiling the opportunities of this distributed ledger technology.

Ready to step into the future?

Blockchain Demystified

Imagine a digital ledger, transparent and immutable, where transactions are recorded for eternity.

That’s blockchain for you, in a nutshell.

Blockchain is a distributed series of digital “blocks” containing transaction records.

Each block is linked together with the one before and after, creating an unbreakable and transparent chain.

Here’s the kicker: once information is recorded, it’s nearly impossible to tamper with.

It’s like writing something in pen, not pencil.

Permanent, secure, and transparent.

Every time a transaction occurs, it’s recorded on a block.

Multiple transactions create a page of this ‘digital ledger.’

When a page is filled, it forms a new block.

Each block is then verified by multiple computers on the network, often referred to as nodes.

Once verified, the block is added to the chain.

Voila!

The transaction is recorded, secure, and visible for anyone to see.

While transactions on the blockchain are visible, the people’s identities are protected by using cryptography.

So, your secrets are safe on blockchain systems, while the transactions are transparent.

It’s like having your cake and eating it too!

This technology isn’t just the backbone of cryptocurrencies like Bitcoin and Ethereum.

Oh no, it’s finding its way into various sectors using a traditional database- healthcare, finance, supply chain, and beyond.

New to crypto trading? Know What is Bitcoin ETF?

The Genesis of Blockchain: A Historical Perspective

Now, let’s hit the rewind button and stroll down memory lane.

Where did blockchain technology first sprout its digital roots?

Buckle up because we’re about to embark on a journey of the history of blockchain protocol.

Although blockchain became mainstream with Bitcoin, its roots can be traced back to the early ‘90s.

Cryptographers had been toying with the idea of a secure, digital ledger for years.

Blockchain is distributed like a tree data structure for storing data by linking blocks using cryptography.

Stuart Haber and W. Scott Stornetta used Merkle trees to implement a system in which document timestamps could not be tampered with.

This was the first instance in the history of blockchain.

Then came 2008.

The world was in the grip of a financial crisis, trust in traditional banking systems was plummeting, and an anonymous entity named Satoshi Nakamoto introduced Bitcoin out of the chaos.

But this story is about the revolutionary technology that powered it – a blockchain database.

Blockchain would be the golden ticket that made Bitcoin a reality.

It provided a secure, transparent, and decentralized method of recording transactions as data on the blockchain.

A private blockchain platform was a game changer in a world where trust was as scarce as a hen’s teeth.

Fast forward to today, and blockchain is no longer just the unsung hero behind cryptocurrencies.

It’s stepping into the limelight, promising to transform industries and economies across the globe if the conditions are met.

And trust me, you’ll want a front-row seat to this show.

Cryptocurrency: The First Blockchain Application

Imagine a world where financial transactions are as transparent as glass, yet as secure as a vault.

That’s the magic cryptocurrency brought to the table.

And guess what?

It’s all thanks to the wizardry of blockchain technology.

Bitcoin, the name that echoed around the world, was the first kid on the blockchain block.

Launched in 2009 by the enigmatic Satoshi Nakamoto, it promised a new era of financial transactions.

But how, you ask?

Well, every Bitcoin transaction ever made is recorded on a blockchain.

It’s like having a public library where anyone can read a book, but no one can edit or delete it.

Transparent, yet secure. Bitcoin was just the opening act.

Soon, other cryptocurrencies like Ethereum, Ripple, and Litecoin joined the party, each bringing its unique flavor to the mix.

At the heart of each was blockchain, ensuring every transaction was as open as a book and as secure as Fort Knox.

Cryptocurrencies aren’t just digital coins to be hoarded like a dragon’s treasure like your private key is.

They’re a means of exchange, a store of value, and a unit of account.

No middlemen, no hefty fees, no waiting periods. It’s financial freedom at the tip of your fingers.

In the grand theatre of financial evolution, blockchain can also be the stage, and cryptocurrencies and crypto futures exchanges are the performers, each playing a pivotal role in this unfolding drama.

Welcome to the brave new world of decentralized finance, where blockchain and cryptocurrencies are not just participants but the show’s directors.

Recommended Read: Common crypto trading mistakes

How Blockchain Powers Cryptocurrencies

Blockchain is like a digital ledger, but not just any ledger.

Imagine a book that’s not stored in one place but is duplicated across a network of computers, a book that’s not controlled by a single entity but is accessible to anyone who wants a peek.

It’s decentralized, distributed, and darn near tamper-proof.

Now, let’s throw cryptocurrencies into the mix.

Every time you send or receive digital coins, that transaction is broadcast to a network of computers, or nodes if we’re getting technical.

These nodes have one job – to validate your transaction. Every node has its own copy of the ledger which is a copy of the blockchain.

It’s like having a team of auditors at your beck and call, ensuring everything is above board.

These transactions aren’t just validated willy-nilly.

They have to be verified and added to a block. This block is then added to a chain of existing blocks.

Hence the name, blockchain.

Now, you might be wondering, “What’s stopping someone from tampering with the block?”

Each block is encrypted and linked to the previous one. Change a block, and you change the entire chain.

However, with blockchain, changing a block is next to impossible. It’s security on steroids.

And here’s the cherry on top.

Every transaction is public, traceable, and permanent.

In the world of cryptocurrencies, blockchain is the unsung hero.

It’s the engine under the hood, the wind beneath the wings.

It ensures that every Bitcoin, Ethereum, or any other digital coin transaction is secure, transparent, and immutable.

In a world teeming with digital innovations, blockchain stands tall as the cornerstone, turning the dream of decentralized finance into a tangible, touchable reality.

Recommended Read: How do liquidity pools work?

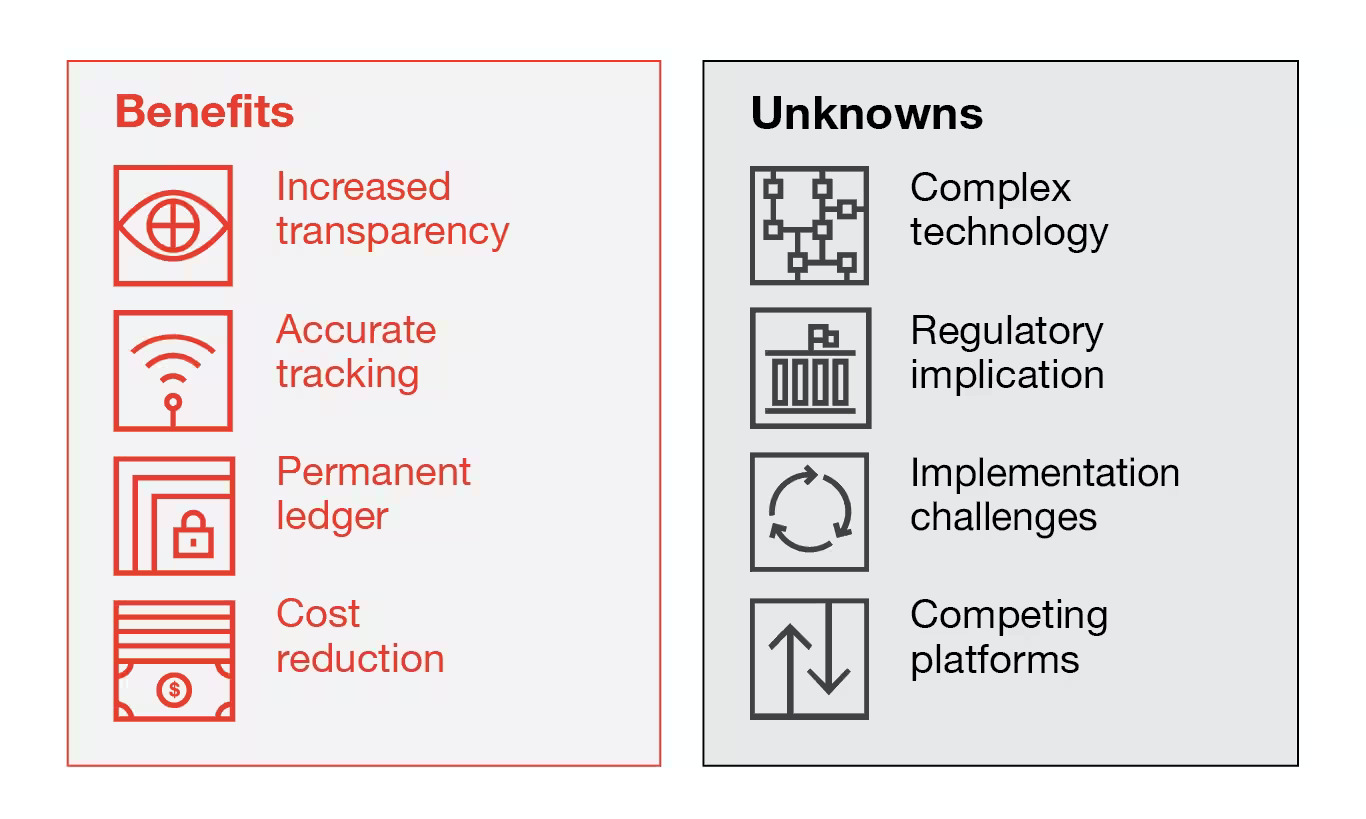

Key Features of Blockchain that Benefit Cryptocurrency

What exactly makes this partnership so powerful?

First off, let’s talk about decentralization.

In the traditional financial world, banks and governments hold the reins.

But in the world of blockchain, there’s no central authority.

It’s like having a democracy where everyone gets a say. This decentralization isn’t just cool; it’s revolutionary.

It means that transactions are peer-to-peer, fast, and efficient.

The blockchain is transparent.

Every transaction is recorded on a public ledger for the world to see.

It’s like having a glass bank where every transaction is visible.

But here’s the kicker – while the transactions are public, the identities of the people making those transactions are encrypted.

And let’s not forget about security. Blockchain uses advanced cryptography to secure transactions.

Transactions are immutable, meaning once they’re recorded, they can’t be altered or deleted.

Blockchain is also highly accessible.

Anyone with an internet connection can make transactions.

It’s like having a bank in your pocket, accessible 24/7, 365 days a year.

It breaks down barriers, making financial transactions accessible to people who don’t have access to traditional banking.

In the grand scheme of things, blockchain is the silent powerhouse that makes cryptocurrencies tick.

It’s the technology that ensures that digital currencies are secure, transparent, and accessible.

In the fast-paced world of digital currencies, blockchain is the anchor, grounding cryptocurrencies and making the magic happen.

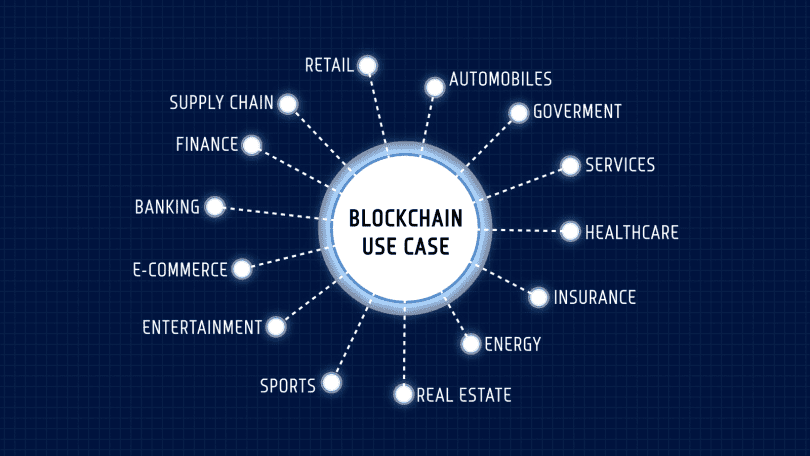

Diverse Applications: Beyond Cryptocurrency

Now, if you can use blockchain technology like a one-trick pony, limited to powering cryptocurrencies, brace yourself for a revelation.

Blockchain could be like a Swiss Army knife.

Intrigued?

Let’s dive deeper.

You can live in a world where supply chains are transparent, where you can use blockchain to track the journey of your coffee from the farm to your cup.

That’s not science fiction; it’s blockchain in action.

In the world of real estate, blockchain is making waves.

Property transactions are notorious for their complexity and paperwork.

Blockchain ensures that property records are immutable and transparent, reducing fraud and making transactions swift and hassle-free.

And in the voting realm, blockchain is the knight in shining armor.

Blockchain introduces a level of transparency and security that makes these issues a thing of the past.

It’s like having a security camera in every ballot box, ensuring that every vote is counted and tamper-proof.

Healthcare, too, isn’t immune to the blockchain revolution.

Patient records are sensitive and private.

Blockchain ensures that these records are stored securely and can be accessed swiftly when needed.

Recommended Read: How does a crypto exchange make money?

Challenges and Criticisms of Blockchain in Crypto

It’s essential to take a step back and consider the challenges and criticisms associated with private blockchains, especially in the realm of cryptocurrency.

Let’s peel back the layers.

First off, scalability is a notorious issue with the use of blockchain.

Did you know Bitcoin and Ethereum grapple with transaction speed and scalability?

It’s a classic case of growing pains, where the increase in users leads to slower transaction times and higher fees.

It’s like a highway during rush hour, where the list of transactions can be completed but it will take some time to be added to the blockchain.

And let’s talk about energy consumption.

For a cryptocurrency miner, especially Bitcoin, this is an energy-intensive process.

The energy consumption of using Bitcoin has raised eyebrows and drawn criticism from environmentalists.

It’s a challenge that’s as real as the digital coins themselves and it remains to be see if it can be solved.

Privacy, or the lack thereof, is another concern.

While the Bitcoin blockchain is praised for its transparency, it’s a double-edged sword.

Every blockchain transaction is recorded and visible to anyone who cares to look at the data stored.

It’s like living in a house with glass walls, where privacy is a luxury.

In a nutshell, while existing blockchain and cryptocurrencies are revolutionary, they aren’t without their challenges.

As we embrace the digital future, addressing these challenges will be pivotal in unlocking blockchain’s full potential in the cryptocurrency space and beyond.

The journey ahead is as exciting as it is uncertain.

Are you ready for the ride?

Future Trajectories: Blockchain and Crypto

Ready for a sneak peek into the future that will be stored on the blockchain?

Let’s fast forward and explore the anticipated trajectories of blockchain and cryptocurrency.

Spoiler alert: it’s as thrilling as a sci-fi odyssey as blockchain technology has many upcoming uses.

Blockchain is not just a buzzword; it’s evolving into a force that could redefine how we perceive decentralized networks, trust, and security in the digital landscape.

Imagine a world where intermediaries are as obsolete as floppy disks, thanks to the decentralized nature of blockchain being used.

It’s not just a pipe dream; it’s a future stored on a blockchain, unfolding before our eyes.

Now, let’s sprinkle some amount of cryptocurrency into the mix. Digital currencies are not just for tech enthusiasts anymore.

They’re making a beeline into the mainstream, and if you think the Bitcoin network made waves with its proof-of-work, brace yourself.

The future promises a plethora of cryptocurrencies like the Ethereum blockchain, each tailored to specific uses and industries.

It’s like having a specialized tool for every task, enhancing efficiency and innovation, rather than a single point of failure.

Integration is the keyword that will dominate whether people use blockchain and crypto.

We’re talking about a seamless blend of blockchain technology into everyday applications, making it as commonplace as smartphones or a traditional database.

Imagine voting in elections, buying property, or accessing healthcare services, all powered by public blockchain and smart contracts without the need for third parties.

Recommended Read: How much bitcoin does the US government own?

Real-World Impacts and Implications

Ever wondered how blockchain and cryptocurrency are not just digital concepts but catalysts sparking real-world transformations?

Hold onto your hats, because we’re about to dive into the tangible impacts and implications that are reshaping our world.

Blockchain is like the silent engine powering a myriad of industries.

Think of it as the unsung hero in sectors like healthcare, where patient data security and accessibility are paramount.

It’s making waves in the supply chain, ensuring transparency and traceability from the manufacturer to your doorstep.

It’s not just about technology; it’s about fostering trust and accountability in every transaction.

Now, let’s shift gears to cryptocurrency. It’s not just a digital asset; it’s a financial revolution.

Imagine sending money across the globe in seconds, not days like some financial institutions.

Envision a world where financial inclusion isn’t a lofty goal but a tangible reality, thanks to the accessibility of cryptocurrencies.

It’s breaking down barriers, making financial empowerment not just a catchphrase but a lived experience.

The decentralized nature of blockchain and the volatility of cryptocurrencies are double-edged swords.

They offer freedom and autonomy but also usher in challenges of security, regulation, and ethical use.

Recommended Read: What to do if your crypto exchange account gets hacked?

Conclusion: The Symbiotic Dance of Blockchain and Crypto

As we wrap up this journey, it’s crystal clear that blockchain and cryptocurrency are more than digital wonders; they’re partners in a dance that’s reshaping our world.

Imagine blockchain as the stage, a foundation of transparency and security, where cryptocurrency performs its swift, unpredictable moves, captivating audiences globally.

But here’s the deal – this dance is evolving.

Every day, new steps are added, and the rhythm changes with innovations and challenges alike.

It’s a performance where technology, economy, and society are not just spectators but active dancers, each influencing the other’s moves.

In the grand finale, the harmony between the benefits of blockchain and cryptocurrency isn’t just about technological advancement but a narrative of transformation, where accessibility, innovation, level of security, and trust take center stage.

Are you ready to join the dance, where every step forward is a leap towards a future reimagined?

The curtain rises, and the next act is ours to choreograph.